It may be tough to obtain a business loan due to strict demands by banks and conventional crediting companies.

But it can be necessary to take out this loan to start or expand your business as well as finance daily costs such as inventory and payroll.

It can be time-consuming to find, apply for, and be approved for a business loan. If you understand your venture’s qualifications, it will be easier to pick the loan that suits your needs.

Here are the 5 steps to help you get a small business loan without hassle.

5 Steps to Obtain a Small Business Loan

Choose the Type of Loan Your Business Needs

Depending on your current financial needs, you may choose one of the lending options suitable for business owners.

- Traditional term loans. These lending tools are suitable for consumers who want to fund a business expansion or a big-ticket purchase. Conventional business loans are issued in a lump sum and can be paid off over time. The interest rate can vary among lenders. You may also choose specific lending tools from some creditors such as loans for vehicle purchases or equipment.

- Business lines of credit. This is a more flexible crediting tool for entrepreneurs who require extra funding for their daily costs. A business line of credit allows you to take a portion of funds each time you want to fulfill a cash need to fund unforeseen repairs or cover the payroll.

- Credit cards. Those who are just starting their venture often don’t get approved for a traditional term loan or a business line of credit. No surprise, as creditors want to see a cash flow to support loan repayment. If you are launching a startup, you may need to use credit cards, borrow money from relatives and friends, or take out a personal loan. You may order an advance check or a balance transfer check from credit card to cover unforeseen expenses, pay for big-ticket purchases in cash, or make payments of different bills. There are some pros and cons of using credit card checks so you should consider your financial situation.

Define If You Qualify for a Business Loan

The next step is to understand why you need a business loan and whether you can qualify for it. Ask yourself about the reason for requesting financial aid.

Are you planning to launch a startup? Do you want to expand your existing venture? Would you like to manage your daily business costs or have a safety cushion?

After that, it’s time to determine your creditworthiness.

You need to know your present credit rating. Get your credit report from one of the credit reporting bureaus to check it for errors and learn what your score is.

In case it’s too low you may need to repair it to maximize your chances of approval. Your FICO score should be at least 690 if you apply to the local bank.

Besides, an entrepreneur should have been in business for a year or more to qualify for traditional term loans while many banks will even require two years.

Finally, you should make enough profit to get approved.

The minimum annual revenue should be from $50,000 to $250,000 for a line of credit and conventional business loan.

Choose the Best Type of Lender

Borrowers may turn to several lending places, including traditional banks, online lenders, and nonprofit microlenders.

Compare your options to select the service provider that best suits your business needs.

- Banks work best for borrowers who have good credit scores, have collateral, and don’t require cash quickly. Banks offer lines of credit and term loans such as the 7(a) loan program. The 7(a) SBA loan program is one of the common lending options for small business owners with special requirements. Those who seek financial aid to refinance present business debt, purchase supplies and furniture, or use the funds for near- and long-term working capital, can submit their application. Borrowers may obtain up to $5 million for their business needs.

- Microlenders work best for borrowers who don’t qualify for a traditional loan as their business is too small. These are nonprofits that can issue up to $35,000. Keep in mind that the interest rates are generally higher compared to bank loans. You should provide financial statements and a business plan to apply.

- Online lenders work best for borrowers who need cash fast, lack time in business, and don’t have collateral. You will be able to obtain between $500 and $500,000 with an APR of up to 108%. The creditors offer more flexible repayment terms but the interest is much higher than at the local banks.

Collect Your Papers

Depending on the service provider, a borrower will need to submit several papers including business and personal tax returns.

business financial statements, business, and personal bank statements, as well as business legal papers (franchise agreement, commercial lease, articles of corporation, etc.)

To be eligible for 7(a) loan assistance, small business packaging ideas should have reasonable invested equity, operate for profit, be able to show a need for a loan.

utilize financial assistance for a business purpose, not have any current debt obligations to the American government, as well as use other financi https://www.theboxprinters.com/small-business-packaging-ideas/al resources before requesting monetary aid.

You will also need to collect financial statements, business financial statements, business certificates or licenses, income tax returns, loan application history, and business leases, and submit a borrower information form (SBA Form 2019).

Apply for a Loan

Make sure you understand all the nuances and repayment terms before you sign the papers.

The US Small Business Administration sets the guidelines that rule the 7(a) loan program.

These lending terms define which businesses may obtain this loan and which loan types they may qualify for.

Link: https://www.sba.gov/partners/lenders/7a-loan-program/terms-conditions-eligibility

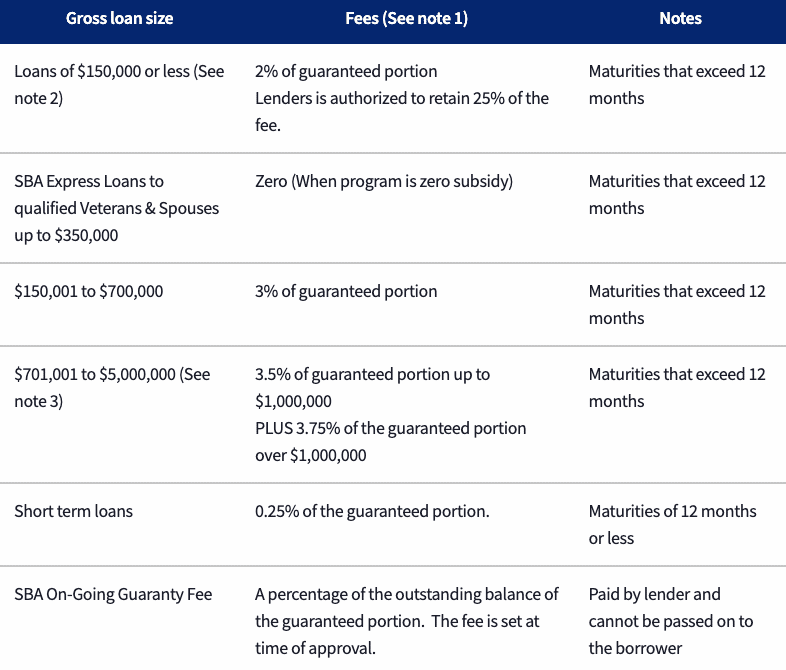

The SBA determines the sum of particular fees every fiscal year for all lending tools approved during that year.

For instance, the guaranty fee on a $100,000 loan with an 85% guarantee would be 2% of $85,000 or $1,700, of which the creditor can retain $425.

The short-term loans have a fee of 0.25% of the guaranteed portion.

Once you are ready and know all the details of the loan you’ve picked, apply for this loan.

The Bottom Line

You should follow this step-by-step guide to facilitate the process of choosing the most suitable business loan.

Once you determine your business’s qualifications and understand your business needs, you will pick the right lending tool.

Related CTN News:

Reasons Why FX Brokers Need Access to Market Liquidity

Stocks to Buy Or Sell Today: 10 Short-Term Trading Ideas by Experts For 17 October 2022

⚠ Article Disclaimer

The above article is sponsored content any opinions expressed in this article are those of the author and not necessarily reflect the views of CTN News